Strategies for Investing in Advanced Energy Technologies in the Decarbonization Era

2023/11/06

The global shift towards decarbonization is driving more investments in cutting-edge energy technologies. However, achieving breakthroughs in the energy sector demands large-scale and long-term financial commitments, including capital investments. This necessitates investment strategies that differ from traditional sectors like IT.

Plug and Play Japan hosted a roundtable featuring the representatives of Energy & Environment Investment, Inc. and the CVC division at ENEOS Holdings Corporation. This discussion centered on current trends and their views on investing in next-generation energy technologies.

(This article is based on the roundtable discussion at the Japan Summit Summer/Fall 2023 on September 15, 2023)

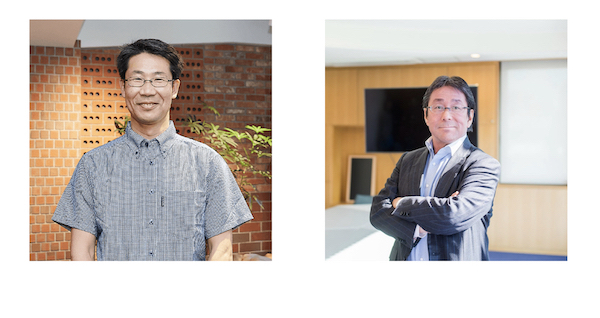

Shuichi Kawamura

President Energy & Environment Investment, Inc. (photo on the left)

Takahiro Ohmachi

Deputy General Manager Emerging Business Development ENEOS Holdings, Inc. (photo on the right)

Moderator: Kathy Liu

Plug and Play Director, Energy / SmartCities

Strategy for Investing in the Decarbonization Era

--What kind of technologies are you focusing on lately and why?

- Omachi:

Our business has been relying on oil, and our annual CO2 emissions across Scopes 1, 2, and 3 are reaching approximately 210 million tons. An immediate action towards decarbonization has become essential. Currently, we are focusing on renewable energy, exploring not only wind and solar energies but also the potential of next-generation energies such as SAF (Sustainable Aviation Fuel).

So far, our business growth has been driven by in-house R&D. However, we recognize that it is crucial to enhance open innovation and foster collaborations with other entities in the realm of decarbonization and next-generation energy technologies. This is the reason behind our Central Technology Research Laboratory exploring long-term technologies and their integration with proprietary technologies.

Our role as a CVC is to catalyze open innovation with independent authority and a streamlined system for swift investment decisions. Regarding investment targets, it’s essential to strike a balance between long-term technologies and short-term business development, as well as the equilibrium between the early and middle stages. Hence, we believe that diversification and appropriate evaluations are required.

We make decisions based on the flow of funds and prevailing market trends rather than by the characteristics of the technology itself. We diversify our portfolios and align our investments accordingly.

In terms of fund flows, we observe two different movements: one is structural and other is cyclical. Cyclical flows show periodic surges, like the hydrogen bubble we saw two years ago.

On the structural side, there is an emerging trend where venture capitals in the U.S. are increasingly investing in technologies that have been tested affordably in Europe and then rolled out in the U.S. market. This pattern might indicate a broader structural shift. By examining these dual fund flows, we can glean insights into overarching market trends.

How to project an investment scenario

--How do you approach next-generation technologies which take a longer time to get a return?

- Kawamura:

We are a purely financial entity, and we make‘Impact Investments’which generate positive social and environmental impact alongside a financial return This strategy entails measuring,reporting and managing the societal and environmental impact such as CO2 emissions resulting from the activities of our portfolio companies as well as supporting their growth.

Balancing investments between short-term carbon reduction initiatives and technologies poised to make significant long-term impacts presents a considerable challenge. While we contemplate investments in tried-and-true technologies that consistently reduce carbon emissions, we simultaneously consider investing in advancing technologies and projects aimed at 2050. However, to assess their worth properly, we must take various factors into account such as the potential decline in CO2 emissions resulting from these technologies and projects, the likelihood of their success, and so on.

Although forecasting the future with its myriad potential scenarios is inherently challenging, we need to strategically channel our funds into what we call “moonshots.” We don’t think we can assess the potential of those technologies. Instead, we rely on experts’ insights and market trajectories to make decisions. Meanwhile, what we put the most importance on is the vision and zeal of entrepreneurs. We assess their passion, their team-building prowess, and their capability to build a company that scales.

In terms of market dynamics, we have devised our speculative scenarios for projection. We categorize scenarios into Level 1, Level 2, and Level 3, weighing the risk and probability of each. Level 1 scenarios, which we perceive as highly likely to materialize in the near future, constitute approximately 50% of our investments. Level 2 represents medium-term risk scenarios, making up about 30% of our investments. Lastly, Level 3 encompasses long-term, hard-to-predict scenarios, accounting for roughly 20% of our investments, including so-called “moonshot” technologies with high-risk.

Financial Returns vs Strategic Returns

--How do you balance between financial returns and strategic returns?

- Omachi:

In the realm of CVC, the central challenge lies in striking a balance between strategic and financial returns. While some CVCs are solely driven by strategic returns, we contend that such an approach isn’t sustainable in the long run due to the potential erosion of capital gains. Our CVC is steadfast in its pursuit of financial returns. Our objective is to secure consistent financial returns, underpinned by a collective commitment to cover the company’s cost of capital, ensuring its sustainable operation.

In terms of deriving strategic returns, our emphasis is on augmenting our existing business units with new ventures, a core mandate of CVCs. Instead of relegating the PoC (Proof of Concept) to these business units, we prioritize fostering a symbiotic relationship between them and our portfolios. We also see a significant importance on environmental initiatives, exploring new ways to gain carbon credits besides forests and oceans. This is also an integral part of our strategic return strategy.

- Kawamura:

For us, as a VC, the primary metric is financial returns. However, beyond mere financial gains, we also see importance in generating positive impact. Our focus is on enterprises driven to address societal challenges and amplify their global impact through scalability, all the while anchored by the anticipation of financial dividends from our investments. Straddling the fine line between financial yield and societal contribution is no easy feat. Yet, given the expectations of our investors, we are compelled to navigate this delicate balance.

Strength and Complementary Relationships between CVC and VC

--What are the challenges you see from the point of view of VC and CVC?

- Omachi:

While we recognize the paramount importance of identifying new technologies and forging partnerships, we are acutely aware of the scarcity of seasoned capitalists. Since the inception of our CVC in 2019, we have onboarded one investor with prior CVC experience. We foresee a pressing need to augment our team with more professionals in this domain.

Traditional VCs and capitalists have seen the industry shifts over extended durations, amassing invaluable insights and expertise. On the other hand, CVCs tend to have frequent personnel turnovers. I see the strengths of traditional VCs and the inherent challenges of CVCs are complementary. It’s imperative for CVCs to adopt a long-term vision and ensure sustained operations.

- Kawamura:

The biggest challenge we have is the stipulation that mandates an Exit within a decade. In this regard, we can’t help but envy the operational flexibility CVCs are allowed to have. Addressing projects like nuclear fusion, which inherently demand a timeline exceeding 10 years to yield tangible outcomes, poses a significant hurdle for a VC. We are constantly exploring innovative strategies to navigate this constraint.

When comparing things, it is difficult to pick out the best. For instance, evaluating the relative merits of various startups at a specific juncture doesn’t necessarily yield a clear frontrunner. Yet, with the benefit of prolonged industry engagement, we can gauge the potential of startups relative to past contenders. A distinct advantage we VCs hold is our longstanding industry presence, enabling us to cultivate a vast network and garner diverse opinions on myriad businesses and technologies. We are staunch believers in the immense value of sustained commitment, a sentiment we feel resonates with all operational entities, be it CVCs or traditional VCs.

Plug and Play Japan will continue to provide articles covering innovative energy industry trends, the latest technologies, case studies, and more in the future. Stay tuned!